Scott Brinker and Frans Riemersma have debuted the 2022 edition of their marketing technology supergraphic to coincide with this year’s International Martech Day, highlighting nearly 10,000 vendors across the ecosystem.

The latest lumascape comes two years after the last attempt to try and understand the breadth of technologies in the marketing sphere. This time, US-based Brinker has connected up with Riemersma, who has been building out a European martech supergraphic, in order to present an even more comprehensive picture.

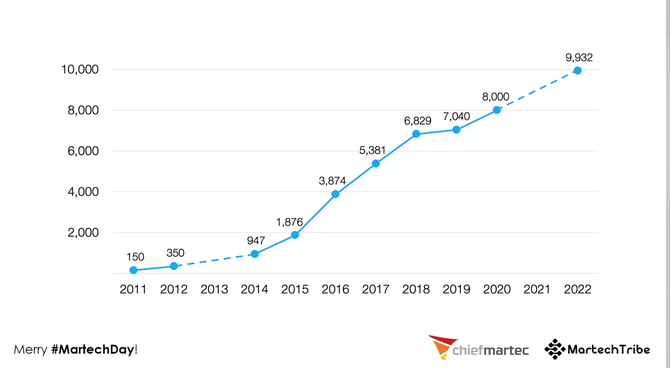

The latest supergraphic from Chiefmartech and MartechTribe highlights 9932 vendors across 49 categories, up from 8000 in 2020, 7040 in 2019 and just 150 back on the original edition of the graph in 2011. This reflects a growth rate of 5233 per cent across a 10-year period.

In a sign of how rapid change across the martech ecosystem continues to occur, the pair also noted 972 exits over the past two years due to acquisitions or unsuccessful product launches. Yet the growth in new martech solutions continues to outpace such exists, albeit at slower growth rates than in previous years.

Prior to completing the new graphic, Brinker estimated the industry had reached 10,000 vendors.

“From the very first one, the moment I come out with the landscape, the analyst community and others comment on how oversaturated it is, and how it’ll radically consolidate and won't be this big ever again. And of course, next year it's even bigger,” Brinker stated.

Categories of technology incorporated into the new-look supergraphic sit under six pillars: Advertising and promotion (1065 vendors); content and experience (2592); social and relationships (2305); commerce and sales (1623); data (1346); and management (1001). Across these, the fastest growth was across content, which climbed up from 1936 to 2592 vendors in one year.

The second biggest category behind content is social and relationships, which Brinker and Riemersma said showed the increasing importance of community and engagement within an audience.

Within these are a wealth of subsets each featuring multiple brands. These stretch from display and programmatic advertising, influencer, search, social, video and affiliate marketing to content marketing, account-based marketing (ABM), marketing automation and campaign/lead management, marketing analytics and attribution, audience data enhancement, business intelligence, customer experience service and success, email marketing, mobile marketing, sales automation and enablement, CRM, CMS and Web experience management, digital asset management (DAM), channel and local marketing, ecommerce, data management platforms (DMPs), customer data platforms (CDPs), data visualisation and reporting, product management, optimisation, personalisation and testing, live chat, talent management, loyalty and referrals, governance and privacy compliance, event/webinar/meetings and interactive content.

Martech continues to consolidate, but the challenge is that it’s doing so in a macro environment, with apps and services appearing in the cloud at a rapid rate, Brinker said. In the sister State of Martech 2022 report, the pair estimated the global market for marketing technology is worth over 344 billion Euros.

“New companies are able to stand on the shoulders of giants,” Brinker said. “The consolidated apps facilitate custom, smaller-scale apps. Customers are able to discover the more personalised, customised apps using these 'giants', leading to higher availability of apps. So, ironically, consolidation is often a catalyst for new software to be created.”

Brinker noted the incredibly long tail of specialist apps, many of which will plug into larger app platforms as extensions rather than standalone applications.

“There is tremendous consolidation at the bottom of this spectrum with those cloud platforms, where four companies hold the majority of the market share,” he continued. “At the top of the spectrum, however, there are millions of custom-built apps and websites. As we go up this spectrum, diversity increases, with each layer building on the ones below.”

It’s also clear organisations and individuals are using more SaaS apps than ever. Latest estimates from Gartner suggested worldwide spend on SaaS will grow 18 per cent this year, from US$145 billion in 2021 to $172 billion in 2022.

“Martech is simply one category of SaaS in which this phenomenon is happening — albeit a relatively large one,” Brinker and Riemersma said. “The same pattern holds across salestech, fintech, devops stacks and so on.”

Brinker and Riemersma have made the landscape a dynamic grid using the favicons from each listed vendor’s website and said they can now publish new versions any time with refreshed data using algorithms.

“Given that the martech industry is likely to continue to evolve rapidly, we will update it regularly,” the pair said, adding industry professionals are now welcome to contribute changes to existing vendors or new additions.

In the third and final episode of our 3-part CMO50 video series exploring modern marketing and why it’s become a matter of trust, we’re delighted to be joined by Telstra’s former CMO and now digital services and sales executive, Jeremy Nicholas, and Adobe VP Marketing Asia-Pacific and Japan, Duncan Egan.

Flash back to the classic film, Willy Wonka and the Chocolate Factory. Television-obsessed Mike insists on becoming the first person to be ‘sent by Wonkavision’, dematerialising on one end, pixel by pixel, and materialising in another space. His cinematic dreams are realised thanks to rash decisions as he is shrunken down to fit the digital universe, followed by a trip to the taffy puller to return to normal size.

Why is it there is no shortage of leadership development materials, yet outstanding leadership is so rare? Despite having access to so many leadership principles, tools, systems and processes, why is it so hard to develop and improve as a leader?

As a nation united by sport, brands are beginning to learn money alone won’t talk without aligned values and action. If recent events with major leagues and their players have shown us anything, it’s the next generation of athletes are standing by what they believe in – and they won’t let their values be superseded by money.